Financial Results for the Quarter Ended March 31, 2024

- For the quarter ended March 31, 2024, net loss attributable to common shareholders was $27.4million, or $0.22 per diluted share, compared to net loss attributable to common shareholders of $44.9million, or $0.36 per diluted share for the same period in 2023.

Non-GAAP Financial Measures

- Core Funds from Operations (“Core FFO”) for the quarter ended March 31, 2024, was $1.19 per common share and dilutive convertible securities (“Share”), as compared to $1.23 for the same period in 2023.

- Same Property Net Operating Income (“NOI”)

- North American, Same Property NOI increased by 7.9% for the quarter ended March 31, 2024, as compared to the corresponding period in 2023.

- UK Same Property NOI increased $3.3 million, or 44.5%, for the quarter ended March 31, 2024, as compared to the corresponding period in 2023.

“The first quarter results demonstrated a strong start to the year as we achieved solid same property NOI growth in the quarter, showcasing the resiliency of our portfolio,” said Gary A. Shiffman, Chairman, President and CEO. “Our performance highlights the quality of the portfolio and the favorable fundamentals underpinning our asset classes, driven by consistent demand in a supply constrained environment. We are intently focused on realizing the dependable growth embedded in our portfolio and confident that we are positioned to drive reliable earnings growth and value creation over the long-term.”

OPERATING HIGHLIGHTS

North America Portfolio Occupancy

- MH and annual RV sites were 97.5% occupied at March 31, 2024, as compared to 96.9% at March 31, 2023.

- Transient-to-annual RV site conversions totaled 176 sites during the first quarter of 2024 and accounted for 75.5% of revenue producing site gains.

Same Property Results

For the properties owned and operated by the Company since at least January 1, 2023, the following table reflects the percentage changes for the quarter ended March 31, 2024:

| Quarter Ended March 31, 2024 | ||||||||||||||

| North America | ||||||||||||||

| MH | RV | Marina | Total | UK | ||||||||||

| Revenue | 6.8 | % | 3.1 | % | 7.1 | % | 6.0 | % | 12.3 | % | ||||

| Expense | 3.4 | % | (1.8)% | 6.5 | % | 2.2 | % | (1.7)% | ||||||

| NOI | 8.0 | % | 8.1 | % | 7.5 | % | 7.9 | % | 44.5 | % | ||||

| Number of Properties | 291 | 165 | 127 | 583 | 53 | |||||||||

Same Property adjusted blended occupancy for MH and RV increased by 180 basis points to 98.9% at March 31, 2024, from 97.1% at March 31, 2023.

INVESTMENT ACTIVITY

During the quarter ended March 31, 2024, the Company:

- Sold two operating communities located in Florida and Arizona with 533 developed sites in aggregate for total cash consideration of approximately $51.7million. The gain from the sale of the properties was $6.2million.

- Expanded one existing community by approximately 30 sites and delivered 70 sites at one ground-up development property.

- Acquired two land parcels located in the U.S. for an aggregate purchase price of $12.9million. In conjunction with one of the acquisitions, the Company issued 4,452 common OP units valued at $0.6million.

Subsequent to the quarter, the Company acquired three marina properties for total consideration of $12.0 million. In conjunction with one of the acquisitions, the Company issued 19,326 common OP units valued at $2.5million.

BALANCE SHEET, CAPITAL MARKETS ACTIVITY AND OTHER ITEMS

As of March 31, 2024, the Company had $7.9 billion in debt outstanding with a weighted average interest rate of 4.2% and a weighted average maturity of 6.8 years. At March 31, 2024, the Company’s net debt to trailing twelve-month Recurring EBITDA ratio was 6.1 times.

During the quarter, the Company:

- Issued $500.0 million of senior unsecured notes with an interest rate of 5.5%, due January 15, 2029, and received net proceeds of $495.4million, after deducting underwriters’ discounts and estimated offering expenses. The majority of the net proceeds were used to reduce floating-rate debt.

2024 GUIDANCE

The Company is updating full year, and establishing second quarter, 2024 guidance for diluted EPS and Core FFO per Share as follows:

| Full Year Ending December 31, 2024 | Second Quarter Ending June 30, 2024 | |||||||||||||||||||||||

| Prior FY Guidance | Revised FY Range | |||||||||||||||||||||||

| Reconciliation of Diluted EPS to Core FFO per Share | Low | High | Low | High | Low | High | ||||||||||||||||||

| Diluted EPS | $ | 2.08 | $ | 2.28 | $ | 1.89 | $ | 2.05 | $ | 0.61 | $ | 0.69 | ||||||||||||

| Depreciation and amortization | 5.35 | 5.35 | 5.45 | 5.45 | 1.33 | 1.33 | ||||||||||||||||||

| Gain on sale of assets | (0.30 | ) | (0.30 | ) | (0.34 | ) | (0.34 | ) | (0.10 | ) | (0.10 | ) | ||||||||||||

| Distributions on preferred OP units | 0.10 | 0.10 | 0.10 | 0.10 | 0.02 | 0.02 | ||||||||||||||||||

| Noncontrolling interest | 0.10 | 0.10 | 0.09 | 0.09 | 0.03 | 0.03 | ||||||||||||||||||

| Transaction costs and other non-recurring G&A expenses | 0.07 | 0.07 | 0.14 | 0.14 | 0.02 | 0.02 | ||||||||||||||||||

| Deferred tax benefit | (0.18 | ) | (0.18 | ) | (0.18 | ) | (0.18 | ) | (0.05 | ) | (0.05 | ) | ||||||||||||

| Difference in weighted average share count attributed to dilutive convertible securities | (0.11 | ) | (0.11 | ) | (0.09 | ) | (0.09 | ) | (0.03 | ) | (0.03 | ) | ||||||||||||

| Other adjustments(a) | (0.07 | ) | (0.07 | ) | — | — | — | — | ||||||||||||||||

| Core FFO(b)(c) per Share | $ | 7.04 | $ | 7.24 | $ | 7.06 | $ | 7.22 | $ | 1.83 | $ | 1.91 | ||||||||||||

(a) Other adjustments consist primarily of remeasurement (gains) / losses, contingent legal and insurance gains and other items presented in the table that reconciles Net loss attributable to SUI common shareholders to Core FFO on page 6.

(b) The diluted share counts for the quarter ending June 30, 2024 and the year ending December 31, 2024 are estimated to be 129.6 million.

(c) The Company’s updated guidance translates forecasted results from operations in the UK using the relevant exchange rate in effect provided in the table presented below. The impact of fluctuations in Canadian and Australian foreign currency rates on revised and initial guidance are not material.

| Exchange Rates in Effect at: | December 31, 2023 | March 31, 2024 | ||

| U.S. Dollar (“USD”) / Pound Sterling (“GBP”) | 1.27 | 1.26 | ||

| USD / Canadian Dollar (“CAD”) | 0.75 | 0.74 | ||

| USD / Australian Dollar (“AUS”) | 0.68 | 0.65 |

The Company’s updated guidance for the full year ending December 31, 2024 is reflected below. Note that certain prior period amounts have been reclassified to conform with current period presentation, with no effect on net income / (loss) and Core FFO. The reclassifications more precisely align certain indirect expenses with underlying activity drivers.

| Same Property Portfolio (in millions and %)(a) | FY 2023 Actual Results | Expected Change in 2024 | |||||

| Prior FY Range | April29, 2024 Update | ||||||

| North America | |||||||

| Revenues from real property | $ | 1,734.6 | 6.4% – 6.8% | 5.4% – 5.8% | |||

| Total property operating expenses | $ | 582.3 | 8.1% – 9.1% | 6.0% – 7.0% | |||

| Total North America Same Property NOI(b)(c) | $ | 1,152.3 | 5.0% – 6.2% | 4.6% – 5.8% | |||

| MH NOI (291 properties) | $ | 607.9 | 6.0% – 7.0% | 6.2% – 7.1% | |||

| RV NOI (165 properties) | $ | 291.7 | 2.1% – 3.5% | (0.3)% – 1.3% | |||

| Marina NOI (127 properties) | $ | 252.7 | 6.1% – 7.5% | 6.4% – 7.6% | |||

| UK (53 properties) | |||||||

| Revenues from real property | $ | 137.9 | 4.8% – 5.4% | 6.4% – 7.0% | |||

| Total property operating expenses | $ | 68.7 | 7.4% – 8.4% | 6.0% – 6.9% | |||

| Total UK Same Property NOI(b) | $ | 69.2 | 1.3% – 3.3% | 6.0% – 8.0% | |||

For the second quarter ending June 30, 2024, the Company’s guidance range assumes North America Same Property NOI growth of 3.4% – 4.9% and UK Same Property NOI growth of 2.5% – 5.0%.

| Consolidated Portfolio Guidance For 2024 (in millions and %) | FY 2023 Actual Results | Expected Change / Range in 2024 | |||||

| Prior FY Range | April29, 2024 Update | ||||||

| Revenues from real property | $ | 2,059.8 | 7.1% – 7.6% | 6.3% – 6.6% | |||

| Total property operating expenses | $ | 810.4 | 8.1% – 8.4% | 5.7% – 6.0% | |||

| Total Real Property NOI | $ | 1,249.4 | 6.3% – 7.3% | 6.5% – 7.3% | |||

| Service, retail, dining and entertainment NOI | $ | 68.5 | $58.4 – $63.2 | $63.0 – $67.0 | |||

| Interest income | $ | 45.4 | $17.6 – $18.6 | $17.8 – $18.8 | |||

| Brokerage commissions and other, net(d)(e) | $ | 60.6 | $44.8 – $47.2 | $37.6 – $39.6 | |||

| FFO contribution from North American home sales | $ | 17.0 | $14.4 – $15.9 | $13.0 – $13.9 | |||

| FFO contribution from UK home sales(f) | $ | 59.2 | $62.3 – $69.9 | $55.4 – $62.4 | |||

| Income from nonconsolidated affiliates | $ | 16.0 | $13.7 – $14.7 | $11.1 – $11.9 | |||

| General and administrative expenses(g) | $ | 272.1 | $262.2 – $267.4 | $269.7 – $274.7 | |||

| Interest expense | $ | 325.8 | $356.3 – $362.7 | $355.6 – $361.1 | |||

| Current tax expense | $ | 14.5 | $14.6 – $16.8 | $13.2 – $14.8 | |||

| Expected Range in FY 2024 |

| Seasonality | 1Q24 | 2Q24 | 3Q24 | 4Q24 | ||||||||

| North America Same Property NOI: | ||||||||||||

| MH | 25 | % | 25 | % | 25 | % | 25 | % | ||||

| RV | 17 | % | 25 | % | 41 | % | 17 | % | ||||

| Marina | 19 | % | 26 | % | 31 | % | 24 | % | ||||

| Total | 22 | % | 25 | % | 30 | % | 23 | % | ||||

| UK Same Property NOI | 14 | % | 25 | % | 40 | % | 21 | % | ||||

| Home Sales FFO | ||||||||||||

| North America | 11 | % | 40 | % | 29 | % | 20 | % | ||||

| UK | 17 | % | 31 | % | 33 | % | 19 | % | ||||

| Consolidated Service, Retail, Dining and Entertainment NOI | 3 | % | 37 | % | 46 | % | 14 | % | ||||

| Consolidated EBITDA | 18 | % | 27 | % | 33 | % | 22 | % | ||||

| Core FFO per Share | 17 | % | 26 | % | 35 | % | 22 | % | ||||

| Footnotes to 2024 Guidance Assumptions | |||||

| (a) | The amounts in the Same Property Portfolio table reflect constant currency, as Canadian and Pound Sterling currency figures included within the 2023 amounts have been translated at the assumed exchange rates used for 2024 guidance. | ||||

| (b) | Total North America Same Property results net $112.2 million and $115.0 million of utility revenue against the related utility expense in property operating expenses for 2023 results and 2024 guidance, respectively. Total UK Same Property results net $16.8 million and $17.7 million of utility revenue against the related utility expense in property operating expenses for 2023 results and 2024 guidance, respectively. | ||||

| (c) | 2023 North America Same Property actual results exclude $0.4 million of expenses incurred at recently acquired properties to bring them up to the Company’s standards. The improvements included items such as tree trimming and painting costs that do not meet the Company’s capitalization policy. | ||||

| (d) | Brokerage commissions and other, net includes $23.4 million of business interruption income for the full year in 2023 and $15.7 million in 2024 for the second through fourth quarters. Expected business interruption recovery for the first quarter of 2024 in the amount of $5.3 million was recorded as an adjustment to Core FFO in the loss of earnings – Catastrophic event-related charges, net line item. | ||||

| (e) | Brokerage commissions and other, net included approximately $8.5 million of lease income in 2023 that will be recognized in total real property NOI in 2024. | ||||

| (f) | Includes UK home sales from Park Holidays and Sandy Bay. | ||||

| (g) | General and administrative in Consolidated Statements of Operations includes $29.6 million and $18.4 million of non-recurring expenses for 2023 results and 2024 updated guidance, respectively. | ||||

The estimates and assumptions presented above represent a range of possible outcomes and may differ materially from actual results. These estimates include contributions from all acquisitions, dispositions and capital markets activity completed through April29, 2024. These estimates exclude all other prospective acquisitions, dispositions and capital markets activity. The estimates and assumptions are forward-looking based on the Company’s current assessment of economic and market conditions and are subject to the other risks outlined below under the caption Cautionary Statement Regarding Forward-Looking Statements.

EARNINGS CONFERENCE CALL

A conference call to discuss first quarter results will be held on Tuesday, April30, 2024 at 2:00 P.M. (ET). To participate, call toll-free at (877) 407-9039. Callers outside the U.S. or Canada can access the call at (201) 689-8470. A replay will be available following the call through May14, 2024 and can be accessed toll-free by calling (844) 512-2921 or (412) 317-6671. The Conference ID number for the call and the replay is 13745022. The conference call will be available live on the Company’s website located at www.suninc.com. The replay will also be available on the website.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This press release contains various “forward-looking statements” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”), and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Company intends that such forward-looking statements will be subject to the safe harbors created thereby. For this purpose, any statements contained in this document that relate to expectations, beliefs, projections, future plans and strategies, trends or prospective events or developments and similar expressions concerning matters that are not historical facts are deemed to be forward-looking statements. Words such as “forecasts,” “intends,” “intend,” “intended,” “goal,” “estimate,” “estimates,” “expects,” “expect,” “expected,” “project,” “projected,” “projections,” “plans,” “predicts,” “potential,” “seeks,” “anticipates,” “anticipated,” “should,” “could,” “may,” “will,” “designed to,” “foreseeable future,” “believe,” “believes,” “scheduled,” “guidance,” “target” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these words. These forward-looking statements reflect the Company’s current views with respect to future events and financial performance, but involve known and unknown risks and uncertainties, both general and specific to the matters discussed in this document, some of which are beyond the Company’s control. These risks and uncertainties and other factors may cause the Company’s actual results to be materially different from any future results expressed or implied by such forward-looking statements. In addition to the risks described under “Risk Factors” contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, and in the Company’s other filings with the Securities and Exchange Commission, from time to time, such risks, uncertainties and other factors include, but are not limited to:

| ∙ | Changes in general economic conditions, including inflation, deflation, energy costs, the real estate industry and the markets within which the Company operates; |

| ∙ | Difficulties in the Company’s ability to evaluate, finance, complete and integrate acquisitions, developments and expansions successfully; |

| ∙ | The Company’s liquidity and refinancing demands; |

| ∙ | The Company’s ability to obtain or refinance maturing debt; |

| ∙ | The Company’s ability to maintain compliance with covenants contained in its debt facilities and its unsecured notes; |

| ∙ | Availability of capital; |

| ∙ | Outbreaks of disease and related restrictions on business operations; |

| ∙ | Changes in foreign currency exchange rates, including between the U.S. dollar and each of the Canadian dollar, Australian dollar and Pound sterling; |

| ∙ | The Company’s ability to maintain rental rates and occupancy levels; |

| ∙ | The Company’s ability to maintain effective internal control over financial reporting and disclosure controls and procedures; |

| ∙ | The Company’s remediation plan and its ability to remediate the material weakness in its internal control over financial reporting; |

| ∙ | Expectations regarding the amount or frequency of impairment losses, including as a result of the write-down of intangible assets, including goodwill; |

| ∙ | Increases in interest rates and operating costs, including insurance premiums and real estate taxes; |

| ∙ | Risks related to natural disasters such as hurricanes, earthquakes, floods, droughts and wildfires; |

| ∙ | General volatility of the capital markets and the market price of shares of the Company’s capital stock; |

| ∙ | The Company’s ability to maintain its status as a REIT; |

| ∙ | Changes in real estate and zoning laws and regulations; |

| ∙ | Legislative or regulatory changes, including changes to laws governing the taxation of REITs; |

| ∙ | Litigation, judgments or settlements, including costs associated with prosecuting or defending claims and any adverse outcomes; |

| ∙ | Competitive market forces; |

| ∙ | The ability of purchasers of manufactured homes and boats to obtain financing; and |

| ∙ | The level of repossessions by manufactured home and boat lenders; |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statement was made. The Company undertakes no obligation to publicly update or revise any forward-looking statements included or incorporated by reference into this document, whether as a result of new information, future events, changes in the Company’s expectations or otherwise, except as required by law.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, the Company cannot guarantee future results, levels of activity, performance or achievements. All written and oral forward-looking statements attributable to the Company or persons acting on the Company’s behalf are qualified in their entirety by these cautionary statements.

Company Overview and Investor Information

The Company

Established in 1975, Sun Communities, Inc. became a publicly owned corporation in December 1993. The Company is a fully integrated REIT listed on the New York Stock Exchange under the symbol: SUI. As of March 31, 2024, the Company owned, operated, or had an interest in a portfolio of 665 developed MH, RV, Marina, and UK properties comprising approximately 180,110 developed sites and approximately 48,040 wet slips and dry storage spaces in the U.S., Canada and the UK.

For more information about the Company, please visit www.suninc.com.

| Company Contacts | |

| Investor Relations | |

| Sara Ismail, Vice President | |

| (248) 208-2500 | |

| investorrelations@suncommunities.com | |

| Corporate Debt Ratings | |

| Moody’s | S&P |

| Baa3 | Stable | BBB | Stable |

| Equity Research Coverage | ||||

| Bank of America Merrill Lynch | Joshua Dennerlein | joshua.dennerlein@bofa.com | ||

| Barclays | Anthony Powell | anthony.powell@barclays.com | ||

| BMO Capital Markets | John Kim | jp.kim@bmo.com | ||

| Citi Research | Eric Wolfe | eric.wolfe@citi.com | ||

| Nicholas Joseph | nicholas.joseph@citi.com | |||

| Deutsche Bank | Conor Peaks | conor.peaks@db.com | ||

| Omotayo Okusanya | omotayo.okusanya@db.com | |||

| Evercore ISI | Samir Khanal | samir.khanal@evercoreisi.com | ||

| Steve Sakwa | steve.sakwa@evercoreisi.com | |||

| Green Street Advisors | John Pawlowski | jpawlowski@greenstreet.com | ||

| JMP Securities | Aaron Hecht | ahecht@jmpsecurities.com | ||

| RBC Capital Markets | Brad Heffern | brad.heffern@rbccm.com | ||

| Robert W. Baird & Co. | Wesley Golladay | wgolladay@rwbaird.com | ||

| Truist Securities | Anthony Hau | anthony.hau@truist.com | ||

| UBS | Michael Goldsmith | michael.goldsmith@ubs.com | ||

| Wells Fargo | James Feldman | james.feldman@wellsfargo.com | ||

| Wolfe Research | Andrew Rosivach | arosivach@wolferesearch.com | ||

| Keegan Carl | kcarl@wolferesearch.com |

Financial and Operating Highlights

($ in millions, except Per Share amounts)

| Quarters Ended | |||||||||||||||||||

| 3/31/2024 | 12/31/2023 | 9/30/2023 | 6/30/2023 | 3/31/2023 | |||||||||||||||

| Financial Information | |||||||||||||||||||

| Basic earnings / (loss) per share(a) | $ | (0.22 | ) | $ | (0.65 | ) | $ | 0.97 | $ | (1.67 | ) | $ | (0.36 | ) | |||||

| Diluted earnings / (loss) per share(a) | $ | (0.22 | ) | $ | (0.65 | ) | $ | 0.97 | $ | (1.68 | ) | $ | (0.36 | ) | |||||

| Cash distributions declared per common share | $ | 0.94 | $ | 0.93 | $ | 0.93 | $ | 0.93 | $ | 0.93 | |||||||||

| FFO per Share(a)(b) | $ | 1.12 | $ | 1.41 | $ | 2.55 | $ | 1.96 | $ | 1.14 | |||||||||

| Core FFO per Share(b) | $ | 1.19 | $ | 1.34 | $ | 2.57 | $ | 1.96 | $ | 1.23 | |||||||||

| Real Property NOI | |||||||||||||||||||

| MH | $ | 162.5 | $ | 155.6 | $ | 153.1 | $ | 151.3 | $ | 150.6 | |||||||||

| RV | 51.2 | 50.4 | 128.2 | 75.6 | 45.1 | ||||||||||||||

| Marina | 56.9 | 65.3 | 83.1 | 72.2 | 52.2 | ||||||||||||||

| UK | 15.3 | 14.0 | 29.0 | 17.3 | 6.4 | ||||||||||||||

| Total | $ | 285.9 | $ | 285.3 | $ | 393.4 | $ | 316.4 | $ | 254.3 | |||||||||

| Recurring EBITDA | $ | 234.0 | $ | 256.0 | $ | 433.0 | $ | 339.7 | $ | 237.4 | |||||||||

| TTM Recurring EBITDA / Interest | 3.7 x | 3.9 x | 4.0 x | 4.3 x | 4.6 x | ||||||||||||||

| Net Debt / TTM Recurring EBITDA | 6.1 x | 6.1 x | 6.1 x | 6.2 x | 6.1 x | ||||||||||||||

| Balance Sheet | |||||||||||||||||||

| Total assets(a) | $ | 17,113.3 | $ | 16,940.7 | $ | 17,246.6 | $ | 17,234.9 | $ | 17,348.1 | |||||||||

| Total debt | $ | 7,872.0 | $ | 7,777.3 | $ | 7,665.0 | $ | 7,614.0 | $ | 7,462.0 | |||||||||

| Total liabilities | $ | 9,830.0 | $ | 9,506.8 | $ | 9,465.0 | $ | 9,474.8 | $ | 9,294.8 | |||||||||

| Operating Information | |||||||||||||||||||

| Properties | |||||||||||||||||||

| MH | 296 | 298 | 298 | 299 | 299 | ||||||||||||||

| RV | 179 | 179 | 182 | 182 | 182 | ||||||||||||||

| Marina | 136 | 135 | 135 | 135 | 135 | ||||||||||||||

| UK | 54 | 55 | 55 | 55 | 55 | ||||||||||||||

| Total | 665 | 667 | 670 | 671 | 671 | ||||||||||||||

| Sites, Wet Slips and Dry Storage Spaces | |||||||||||||||||||

| MH | 99,930 | 100,320 | 100,200 | 100,220 | 100,120 | ||||||||||||||

| Annual RV | 33,290 | 32,390 | 32,150 | 31,620 | 30,860 | ||||||||||||||

| UK | 18,110 | 18,110 | 18,050 | 17,950 | 17,850 | ||||||||||||||

| Transient | 28,780 | 28,490 | 29,770 | 30,270 | 30,870 | ||||||||||||||

| Total sites | 180,110 | 179,310 | 180,170 | 180,060 | 179,700 | ||||||||||||||

| Marina wet slips and dry storage spaces(c) | 48,040 | 48,030 | 48,030 | 48,180 | 47,990 | ||||||||||||||

| Occupancy | |||||||||||||||||||

| MH | 96.7 | % | 96.6 | % | 96.3 | % | 96.2 | % | 96.0 | % | |||||||||

| Annual RV | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||

| Blended MH and annual RV | 97.5 | % | 97.4 | % | 97.2 | % | 97.1 | % | 96.9 | % | |||||||||

| UK | 88.9 | % | 89.5 | % | 90.6 | % | 90.1 | % | 90.1 | % | |||||||||

| MH and RV Revenue Producing Site Net Gains(d) | |||||||||||||||||||

| MH leased sites, net | 57 | 387 | 207 | 285 | 278 | ||||||||||||||

| RV leased sites, net | 176 | 296 | 537 | 754 | 524 | ||||||||||||||

| Total leased sites, net | 233 | 683 | 744 | 1,039 | 802 | ||||||||||||||

(a) As adjusted for Park Holidays non-cash goodwill impairment. Refer to Definitions and Notes for additional information.

(b) Excludes the effect of certain anti-dilutive convertible securities.

(c) Total wet slips and dry storage spaces are adjusted each quarter based on site configuration and usability.

(d) Revenue producing site net gains do not include occupied sites acquired during the year.

Portfolio Overview as of March 31, 2024

| MH & RV Properties | |||||||||||||

| Properties | MH & Annual RV | Transient RV Sites | Total Sites | Sites for Development | |||||||||

| Location | Sites | Occupancy % | |||||||||||

| North America | |||||||||||||

| Florida | 128 | 41,180 | 97.7 | % | 3,950 | 45,130 | 2,950 | ||||||

| Michigan | 85 | 32,950 | 96.9 | % | 580 | 33,530 | 1,290 | ||||||

| California | 37 | 6,920 | 98.8 | % | 1,870 | 8,790 | 850 | ||||||

| Texas | 29 | 9,020 | 96.5 | % | 1,800 | 10,820 | 3,850 | ||||||

| Ontario, Canada | 16 | 4,610 | 100.0 | % | 590 | 5,200 | 1,450 | ||||||

| Connecticut | 16 | 1,910 | 95.0 | % | 90 | 2,000 | — | ||||||

| Maine | 15 | 2,490 | 96.1 | % | 1,050 | 3,540 | 200 | ||||||

| Arizona | 12 | 4,480 | 97.4 | % | 830 | 5,310 | 1,120 | ||||||

| Indiana | 12 | 3,140 | 98.2 | % | 1,030 | 4,170 | 180 | ||||||

| New Jersey | 11 | 2,950 | 100.0 | % | 1,040 | 3,990 | 260 | ||||||

| Colorado | 11 | 2,900 | 87.7 | % | 980 | 3,880 | 1,420 | ||||||

| Virginia | 10 | 1,610 | 99.9 | % | 2,070 | 3,680 | 750 | ||||||

| New York | 10 | 1,510 | 99.2 | % | 1,430 | 2,940 | 780 | ||||||

| Other | 83 | 17,550 | 98.8 | % | 8,250 | 25,800 | 1,000 | ||||||

| Total | 475 | 133,220 | 97.5 | % | 25,560 | 158,780 | 16,100 | ||||||

| Properties | UK Properties | Transient Sites | Total Sites | Sites for Development | |||||||||

| Location | Sites | Occupancy % | |||||||||||

| United Kingdom | 54 | 18,110 | 88.9 | % | 3,220 | 21,330 | 2,410 | ||||||

| Marina | ||||||||

| Properties | Wet Slips and Dry Storage Spaces | |||||||

| Location | ||||||||

| Florida | 21 | 5,150 | ||||||

| Rhode Island | 12 | 3,460 | ||||||

| California | 11 | 5,710 | ||||||

| Connecticut | 11 | 3,330 | ||||||

| New York | 9 | 3,020 | ||||||

| Massachusetts | 9 | 2,560 | ||||||

| Maryland | 9 | 2,480 | ||||||

| Other | 54 | 22,330 | ||||||

| Total | 136 | 48,040 | ||||||

| Properties | Sites, Wet Slips and Dry Storage Spaces | |||||||

| Total Portfolio | 665 | 228,150 |

Consolidated Balance Sheets

(amounts in millions)

| March 31, 2024 | December 31, 2023 | ||||||

| Assets | |||||||

| Land | $ | 4,551.7 | $ | 4,278.2 | |||

| Land improvements and buildings | 11,529.5 | 11,682.2 | |||||

| Rental homes and improvements | 755.9 | 744.4 | |||||

| Furniture, fixtures and equipment | 1,031.3 | 1,011.7 | |||||

| Investment property | 17,868.4 | 17,716.5 | |||||

| Accumulated depreciation | (3,410.5 | ) | (3,272.9 | ) | |||

| Investment property, net | 14,457.9 | 14,443.6 | |||||

| Cash, cash equivalents and restricted cash | 132.5 | 42.7 | |||||

| Inventory of manufactured homes | 191.0 | 205.6 | |||||

| Notes and other receivables, net | 469.1 | 421.6 | |||||

| Collateralized receivables, net(a) | 56.5 | 56.2 | |||||

| Goodwill | 731.4 | 733.0 | |||||

| Other intangible assets, net | 361.7 | 369.5 | |||||

| Other assets, net | 713.2 | 668.5 | |||||

| Total Assets | $ | 17,113.3 | $ | 16,940.7 | |||

| Liabilities | |||||||

| Mortgage loans payable | $ | 3,465.5 | $ | 3,478.9 | |||

| Secured borrowings on collateralized receivables(a) | 56.1 | 55.8 | |||||

| Unsecured debt | 4,350.4 | 4,242.6 | |||||

| Distributions payable | 119.7 | 118.2 | |||||

| Advanced reservation deposits and rent | 480.4 | 344.5 | |||||

| Accrued expenses and accounts payable | 370.4 | 313.7 | |||||

| Other liabilities | 987.5 | 953.1 | |||||

| Total Liabilities | 9,830.0 | 9,506.8 | |||||

| Commitments and contingencies | |||||||

| Temporary equity | 259.7 | 260.9 | |||||

| Shareholders’ Equity | |||||||

| Common stock | 1.2 | 1.2 | |||||

| Additional paid-in capital | 9,471.4 | 9,466.9 | |||||

| Accumulated other comprehensive income | 6.7 | 12.2 | |||||

| Distributions in excess of accumulated earnings | (2,540.6 | ) | (2,397.5 | ) | |||

| Total SUI shareholders’ equity | 6,938.7 | 7,082.8 | |||||

| Noncontrolling interests | |||||||

| Common and preferred OP units | 84.9 | 90.2 | |||||

| Total noncontrolling interests | 84.9 | 90.2 | |||||

| Total Shareholders’ Equity | 7,023.6 | 7,173.0 | |||||

| Total Liabilities, Temporary Equity and Shareholders’ Equity | $ | 17,113.3 | $ | 16,940.7 | |||

(a) Refer to “Secured borrowings on collateralized receivables” within Definitions and Notes for additional information.

Consolidated Statements of Operations

(amounts in millions, except for per share amounts)

| Quarter Ended | ||||||||||

| March 31, 2024 | March 31, 2023 | % Change | ||||||||

| Revenues | As Restated | |||||||||

| Real property (excluding transient)(a) | $ | 435.4 | $ | 398.2 | 9.3 | % | ||||

| Real property – transient | 41.5 | 43.4 | (4.4)% | |||||||

| Home sales | 68.9 | 86.3 | (20.2)% | |||||||

| Service, retail, dining and entertainment | 117.9 | 102.4 | 15.1 | % | ||||||

| Interest | 4.6 | 11.4 | (59.6)% | |||||||

| Brokerage commissions and other, net | 3.0 | 9.5 | (68.4)% | |||||||

| Total Revenues | 671.3 | 651.2 | 3.1 | % | ||||||

| Expenses | ||||||||||

| Property operating and maintenance(a) | 159.7 | 157.2 | 1.6 | % | ||||||

| Real estate tax | 31.3 | 30.1 | 4.0 | % | ||||||

| Home costs and selling | 51.9 | 62.6 | (17.1)% | |||||||

| Service, retail, dining and entertainment | 115.9 | 99.8 | 16.1 | % | ||||||

| General and administrative | 78.5 | 64.1 | 22.5 | % | ||||||

| Catastrophic event-related charges, net | 7.2 | 1.0 | N/M | |||||||

| Business combinations | — | 2.8 | (100.0)% | |||||||

| Depreciation and amortization | 165.3 | 155.6 | 6.2 | % | ||||||

| Asset impairments | 20.7 | 2.4 | N/M | |||||||

| Goodwill impairment | — | 15.4 | (100.0)% | |||||||

| Loss on extinguishment of debt | 0.6 | — | N/A | |||||||

| Interest | 89.7 | 76.6 | 17.1 | % | ||||||

| Interest on mandatorily redeemable preferred OP units / equity | — | 1.0 | (100.0)% | |||||||

| Total Expenses | 720.8 | 668.6 | 7.8 | % | ||||||

| Loss Before Other Items | (49.5 | ) | (17.4 | ) | 184.5 | % | ||||

| Loss on remeasurement of marketable securities | — | (19.9 | ) | (100.0)% | ||||||

| Gain / (loss) on foreign currency exchanges | 1.1 | (2.7 | ) | N/M | ||||||

| Gain / (loss) on dispositions of properties | 5.4 | (1.6 | ) | N/M | ||||||

| Other income / (expense), net(b) | 8.0 | (1.0 | ) | N/M | ||||||

| Loss on remeasurement of notes receivable | (0.7 | ) | (1.7 | ) | (58.8)% | |||||

| Income / (loss) from nonconsolidated affiliates | 1.4 | (0.2 | ) | N/M | ||||||

| Gain / (loss) on remeasurement of investment in nonconsolidated affiliates | 5.2 | (4.5 | ) | N/M | ||||||

| Current tax expense | (2.1 | ) | (3.9 | ) | (46.2)% | |||||

| Deferred tax benefit | 5.7 | 4.6 | 23.9 | % | ||||||

| Net Loss | (25.5 | ) | (48.3 | ) | (47.2)% | |||||

| Less: Preferred return to preferred OP units / equity interests | 3.2 | 2.4 | 33.3 | % | ||||||

| Less: Loss attributable to noncontrolling interests | (1.3 | ) | (5.8 | ) | (77.6)% | |||||

| Net Loss Attributable to SUI Common Shareholders | $ | (27.4 | ) | $ | (44.9 | ) | (39.0)% | |||

| Weighted average common shares outstanding – basic(b) | 123.6 | 123.3 | 0.2 | % | ||||||

| Weighted average common shares outstanding – diluted(b) | 126.6 | 126.2 | 0.3 | % | ||||||

| Basic loss per share | $ | (0.22 | ) | $ | (0.36 | ) | (38.9)% | |||

| Diluted loss per share(c) | $ | (0.22 | ) | $ | (0.36 | ) | (38.9)% | |||

(a) Refer to “Utility Revenues” within Definitions and Notes for additional information.

(b) Refer to Definitions and Notes for additional information.

(c) Excludes the effect of certain anti-dilutive convertible securities.

N/M = Not meaningful.

N/A = Not applicable.

Reconciliation of Net Loss Attributable to SUI Common Shareholders to Core FFO

(amounts in millions, except for per share data)

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| As Restated | |||||||

| Net Loss Attributable to SUI Common Shareholders | $ | (27.4 | ) | $ | (44.9 | ) | |

| Adjustments | |||||||

| Depreciation and amortization | 164.5 | 154.9 | |||||

| Depreciation on nonconsolidated affiliates | 0.1 | — | |||||

| Asset impairments | 20.7 | 2.4 | |||||

| Goodwill impairment | — | 15.4 | |||||

| Loss on remeasurement of marketable securities | — | 19.9 | |||||

| (Gain) / loss on remeasurement of investment in nonconsolidated affiliates | (5.2 | ) | 4.5 | ||||

| Loss on remeasurement of notes receivable | 0.7 | 1.7 | |||||

| (Gain) / loss on dispositions of properties, including tax effect | (5.3 | ) | 3.5 | ||||

| Add: Returns on preferred OP units | 2.1 | 2.1 | |||||

| Add: Loss attributable to noncontrolling interests | (0.9 | ) | (5.7 | ) | |||

| Gain on dispositions of assets, net | (5.4 | ) | (7.9 | ) | |||

| FFO(a) | $ | 143.9 | $ | 145.9 | |||

| Adjustments | |||||||

| Business combination expense | — | 2.8 | |||||

| Acquisition and other transaction costs(a) | 9.9 | 3.7 | |||||

| Loss on extinguishment of debt | 0.6 | — | |||||

| Catastrophic event-related charges, net | 7.2 | 1.0 | |||||

| Loss of earnings – catastrophic event-related charges, net(b) | 5.3 | 5.5 | |||||

| (Gain) / loss on foreign currency exchanges | (1.1 | ) | 2.7 | ||||

| Other adjustments, net(a) | (12.4 | ) | (3.6 | ) | |||

| Core FFO(a)(c) | $ | 153.4 | $ | 158.0 | |||

| Weighted Average Common Shares Outstanding – Diluted | 128.7 | 128.2 | |||||

| FFO per Share(c) | $ | 1.12 | $ | 1.14 | |||

| Core FFO per Share(c) | $ | 1.19 | $ | 1.23 | |||

(a) Refer to Definitions and Notes for additional information.

(b) Loss of earnings – catastrophic event-related charges, net include the following:

| Quarter Ended | |||||

| March 31, 2024 | March 31, 2023 | ||||

| Hurricane Ian – Three Fort Myers, Florida RV communities impaired | |||||

| Estimated loss of earnings in excess of the applicable business interruption deductible | $ | 5.3 | $ | 5.3 | |

| Hurricane Irma – Three Florida Keys communities impaired | |||||

| Estimated loss of earnings in excess of the applicable business interruption deductible | — | 0.2 | |||

| Loss of earnings – catastrophic event-related charges, net | $ | 5.3 | $ | 5.5 | |

(c) Excludes the effect of certain anti-dilutive convertible securities.

Refer to Definitions and Notes for Home sales contribution to FFO.

Reconciliation of Net Loss Attributable to SUI Common Shareholders to NOI

(amounts in millions)

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| As Restated | |||||||

| Net Loss Attributable to SUI Common Shareholders | $ | (27.4 | ) | $ | (44.9 | ) | |

| Interest income | (4.6 | ) | (11.4 | ) | |||

| Brokerage commissions and other revenues, net | (3.0 | ) | (9.5 | ) | |||

| General and administrative | 78.5 | 64.1 | |||||

| Catastrophic event-related charges, net | 7.2 | 1.0 | |||||

| Business combination expense | — | 2.8 | |||||

| Depreciation and amortization | 165.3 | 155.6 | |||||

| Asset impairments | 20.7 | 2.4 | |||||

| Goodwill impairment | — | 15.4 | |||||

| Loss on extinguishment of debt | 0.6 | — | |||||

| Interest expense | 89.7 | 76.6 | |||||

| Interest on mandatorily redeemable preferred OP units / equity | — | 1.0 | |||||

| Loss on remeasurement of marketable securities | — | 19.9 | |||||

| (Gain) / loss on foreign currency exchanges | (1.1 | ) | 2.7 | ||||

| (Gain) / loss on disposition of properties | (5.4 | ) | 1.6 | ||||

| Other (income) / expense, net(a) | (8.0 | ) | 1.0 | ||||

| Loss on remeasurement of notes receivable | 0.7 | 1.7 | |||||

| (Income) / loss from nonconsolidated affiliates | (1.4 | ) | 0.2 | ||||

| (Gain) / loss on remeasurement of investment in nonconsolidated affiliates | (5.2 | ) | 4.5 | ||||

| Current tax expense | 2.1 | 3.9 | |||||

| Deferred tax benefit | (5.7 | ) | (4.6 | ) | |||

| Add: Preferred return to preferred OP units / equity interests | 3.2 | 2.4 | |||||

| Add: Loss attributable to noncontrolling interests | (1.3 | ) | (5.8 | ) | |||

| NOI | $ | 304.9 | $ | 280.6 | |||

| Quarter Ended | |||||

| March 31, 2024 | March 31, 2023 | ||||

| Real property NOI(a) | $ | 285.9 | $ | 254.3 | |

| Home sales NOI (a) | 17.0 | 23.7 | |||

| Service, retail, dining and entertainment NOI(a) | 2.0 | 2.6 | |||

| NOI | $ | 304.9 | $ | 280.6 | |

(a) Refer to Definitions and Notes for additional information.

Reconciliation of Net Loss Attributable to SUI Common Shareholders to Recurring EBITDA

(amounts in millions)

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| As Restated | |||||||

| Net Loss Attributable to SUI Common Shareholders | $ | (27.4 | ) | $ | (44.9 | ) | |

| Adjustments | |||||||

| Depreciation and amortization | 165.3 | 155.6 | |||||

| Asset impairments | 20.7 | 2.4 | |||||

| Goodwill impairment | — | 15.4 | |||||

| Loss on extinguishment of debt | 0.6 | — | |||||

| Interest expense | 89.7 | 76.6 | |||||

| Interest on mandatorily redeemable preferred OP units / equity | — | 1.0 | |||||

| Current tax expense | 2.1 | 3.9 | |||||

| Deferred tax benefit | (5.7 | ) | (4.6 | ) | |||

| (Income) / loss from nonconsolidated affiliates | (1.4 | ) | 0.2 | ||||

| Less: (Gain) / loss on dispositions of properties | (5.4 | ) | 1.6 | ||||

| Less: Gain on dispositions of assets, net | (5.4 | ) | (7.9 | ) | |||

| EBITDAre | $ | 233.1 | $ | 199.3 | |||

| Adjustments | |||||||

| Catastrophic event-related charges, net | 7.2 | 1.0 | |||||

| Business combination expense | — | 2.8 | |||||

| Loss on remeasurement of marketable securities | — | 19.9 | |||||

| (Gain) / loss on foreign currency exchanges | (1.1 | ) | 2.7 | ||||

| Other (income) / expense, net(a) | (8.0 | ) | 1.0 | ||||

| Loss on remeasurement of notes receivable | 0.7 | 1.7 | |||||

| (Gain) / loss on remeasurement of investment in nonconsolidated affiliates | (5.2 | ) | 4.5 | ||||

| Add: Preferred return to preferred OP units / equity interests | 3.2 | 2.4 | |||||

| Add: Loss attributable to noncontrolling interests | (1.3 | ) | (5.8 | ) | |||

| Add: Gain on dispositions of assets, net | 5.4 | 7.9 | |||||

| Recurring EBITDA | $ | 234.0 | $ | 237.4 | |||

(a) Refer to Definitions and Notes for additional information.

Real Property Operations – Total Portfolio

(amounts in millions, except statistical information)

| Quarter Ended March 31, 2024 | Quarter Ended March 31, 2023 | ||||||||||||||||||||||||||||||||||||

| Financial Information | MH | RV | Marinas | UK | Total | MH | RV | Marinas | UK | Total | |||||||||||||||||||||||||||

| Revenues | |||||||||||||||||||||||||||||||||||||

| Real property (excluding transient)(a) | $ | 237.6 | $ | 70.0 | $ | 92.4 | $ | 35.4 | $ | 435.4 | $ | 223.5 | $ | 61.8 | $ | 85.4 | $ | 27.5 | $ | 398.2 | |||||||||||||||||

| Real property – transient | 0.4 | 34.5 | 4.0 | 2.6 | 41.5 | 0.5 | 37.8 | 3.7 | 1.4 | 43.4 | |||||||||||||||||||||||||||

| Total operating revenues | 238.0 | 104.5 | 96.4 | 38.0 | 476.9 | 224.0 | 99.6 | 89.1 | 28.9 | 441.6 | |||||||||||||||||||||||||||

| Expenses | |||||||||||||||||||||||||||||||||||||

| Property operating expenses | 75.5 | 53.3 | 39.5 | 22.7 | 191.0 | 73.4 | 54.5 | 36.9 | 22.5 | 187.3 | |||||||||||||||||||||||||||

| Real Property NOI | $ | 162.5 | $ | 51.2 | $ | 56.9 | $ | 15.3 | $ | 285.9 | $ | 150.6 | $ | 45.1 | $ | 52.2 | $ | 6.4 | $ | 254.3 | |||||||||||||||||

| As of March 31, 2024 | As of March 31, 2023 | ||||||||||||||||||||||||||||||||||||

| Other information | MH | RV | Marinas | UK | Total | MH | RV | Marinas | UK | Total | |||||||||||||||||||||||||||

| Number of properties | 296 | 179 | 136 | 54 | 665 | 299 | 182 | 135 | 55 | 671 | |||||||||||||||||||||||||||

| Sites, wet slips and dry storage spaces | |||||||||||||||||||||||||||||||||||||

| Sites, wet slips and dry storage spaces(b) | 99,930 | 33,290 | 48,040 | 18,110 | 199,370 | 100,120 | 30,860 | 47,990 | 17,850 | 196,820 | |||||||||||||||||||||||||||

| Transient sites | N/A | 25,560 | N/A | 3,220 | 28,780 | N/A | 27,610 | N/A | 3,260 | 30,870 | |||||||||||||||||||||||||||

| Total | 99,930 | 58,850 | 48,040 | 21,330 | 228,150 | 100,120 | 58,470 | 47,990 | 21,110 | 227,690 | |||||||||||||||||||||||||||

| Occupancy | 96.7 | % | 100.0 | % | N/A | 88.9 | % | 96.5 | % | 96.0 | % | 100.0 | % | N/A | 90.1 | % | 96.1 | % | |||||||||||||||||||

N/M = Not meaningful. N/A = Not applicable.

(a) Refer to “Utility Revenues” within Definitions and Notes for additional information.

(b) MH annual sites included 10,300 and 9,520 rental homes in the Company’s Rental Program at March 31, 2024 and 2023, respectively. The Company’s investment in occupied rental homes at March 31, 2024 was $696.3 million, an increase of 15.7% from $601.8 million at March 31, 2023.

Real Property Operations – North America Same Property Portfolio(a)

(amounts in millions, except for statistical information)

| Quarter Ended March 31, 2024 | Quarter Ended March 31, 2023 | Total Change | % Change(c) | ||||||||||||||||||||||||||||||||||||

| MH(b) | RV(b) | Marina | Total | MH(b) | RV(b) | Marina | Total | MH | RV | Marina | Total | ||||||||||||||||||||||||||||

| Financial Information | |||||||||||||||||||||||||||||||||||||||

| Same Property Revenues | |||||||||||||||||||||||||||||||||||||||

| Real property (excluding transient) | $ | 218.0 | $ | 65.1 | $ | 78.9 | $ | 362.0 | $ | 204.1 | $ | 57.4 | $ | 73.5 | $ | 335.0 | $ | 27.0 | 6.8 | % | 13.4 | % | 7.3 | % | 8.0 | % | |||||||||||||

| Real property – transient | 0.4 | 31.3 | 3.9 | 35.6 | 0.4 | 36.0 | 3.7 | 40.1 | (4.5 | ) | 19.0 | % | (13.2)% | 4.9 | % | (11.2)% | |||||||||||||||||||||||

| Total Same Property operating revenues | 218.4 | 96.4 | 82.8 | 397.6 | 204.5 | 93.4 | 77.2 | 375.1 | 22.5 | 6.8 | % | 3.1 | % | 7.1 | % | 6.0 | % | ||||||||||||||||||||||

| Same Property Expenses | |||||||||||||||||||||||||||||||||||||||

| Same Property operating expenses(d)(e) | 56.2 | 46.2 | 31.4 | 133.8 | 54.4 | 47.0 | 29.4 | 130.8 | 3.0 | 3.4 | % | (1.8)% | 6.5 | % | 2.2 | % | |||||||||||||||||||||||

| Real Property NOI(e) | $ | 162.2 | $ | 50.2 | $ | 51.4 | $ | 263.8 | $ | 150.1 | $ | 46.4 | $ | 47.8 | $ | 244.3 | $ | 19.5 | 8.0 | % | 8.1 | % | 7.5 | % | 7.9 | % | |||||||||||||

| Other Information | |||||||||||||||||||||||||||||||||||||||

| Number of properties | 291 | 165 | 127 | 583 | 291 | 165 | 127 | 583 | |||||||||||||||||||||||||||||||

| Sites, wet slips and dry storage spaces | 99,130 | 55,720 | 43,450 | 198,300 | 99,280 | 55,430 | 43,460 | 198,170 | |||||||||||||||||||||||||||||||

(a) Refer to the Definitions and Notes for additional information.

(b) Same Property results for the Company’s MH and RV properties reflect constant currency for comparative purposes. Canadian currency figures in the prior comparative period have been translated at the average exchange rate of $0.7418 USD per Canadian dollar, during the quarter ended March 31, 2024.

(c) Percentages are calculated based on unrounded numbers.

(d) Refer to “Utility Revenues” within Definitions and Notes for additional information.

(e) Total Same Property operating expenses consist of the following components for the periods shown (in millions) and exclude amounts invested into recently acquired properties to bring them up to the Company’s standards:

| Quarter Ended | ||||||||||||

| March 31, 2024 | March 31, 2023 | Change | % Change(c) | |||||||||

| Payroll and benefits | $ | 42.7 | $ | 43.4 | $ | (0.7 | ) | (1.7)% | ||||

| Real estate taxes | 28.8 | 28.0 | 0.8 | 2.5 | % | |||||||

| Supplies and repairs | 15.5 | 14.4 | 1.1 | 7.6 | % | |||||||

| Utilities | 13.9 | 14.5 | (0.6 | ) | (4.7)% | |||||||

| Legal, state / local taxes, and insurance | 14.4 | 14.6 | (0.2 | ) | (0.9)% | |||||||

| Other | 18.5 | 15.9 | 2.6 | 16.9 | % | |||||||

| Total Same Property Operating Expenses | $ | 133.8 | $ | 130.8 | $ | 3.0 | 2.2 | % | ||||

Real Property Operations – North America Same Property Portfolio(a) (Continued)

(amounts in millions, except for statistical information)

| As of | ||||||||||||||||

| March 31, 2024 | March 31, 2023 | |||||||||||||||

| MH | RV | MH | RV | |||||||||||||

| Other Information | ||||||||||||||||

| Number of properties | 291 | 165 | 291 | 165 | ||||||||||||

| Sites | ||||||||||||||||

| MH and Annual RV sites | 99,130 | 32,440 | 99,280 | 30,700 | ||||||||||||

| Transient RV sites | N/A | 23,280 | N/A | 24,730 | ||||||||||||

| Total | 99,130 | 55,720 | 99,280 | 55,430 | ||||||||||||

| MH and Annual RV Occupancy | ||||||||||||||||

| Occupancy(b) | 97.2 | % | 100.0 | % | 96.6 | % | 100.0 | % | ||||||||

| Monthly base rent per site | $ | 686 | $ | 608 | $ | 647 | $ | 567 | ||||||||

| % Change of monthly base rent(c) | 6.0 | % | 7.2 | % | N/A | N/A | ||||||||||

| Rental Program Statistics included in MH: | ||||||||||||||||

| Number of occupied sites, end of period(d) | 10,120 | N/A | 9,500 | N/A | ||||||||||||

| Monthly rent per site – MH Rental Program | $ | 1,312 | N/A | $ | 1,247 | N/A | ||||||||||

| % Change(d) | 5.3 | % | N/A | N/A | N/A | |||||||||||

N/A = Not applicable.

(a) Refer to Definitions and Notes for additional information.

(b) Same Property blended occupancy for MH and RV was 97.9% at March 31, 2024, up 50 basis points from 97.4% at March 31, 2023. Adjusting for recently delivered and vacant expansion sites, Same Property adjusted blended occupancy for MH and RV increased by 180 basis points year over year, to 98.9% at March 31, 2024, from 97.1% at March 31, 2023.

(c) Calculated using actual results without rounding.

(d) Occupied rental program sites in Same Property are included in total sites.

Real Property Operations – UK Same Property Portfolio(a)

(amounts in millions, except for statistical information)

| Quarter Ended | ||||||||

| March 31, 2024 | March 31, 2023 | % Change(c) | ||||||

| Financial Information(b) | ||||||||

| Same Property Revenues | ||||||||

| Real property (excluding transient) | $ | 24.9 | $ | 23.0 | 8.3 | % | ||

| Real property – transient | 2.6 | 1.5 | 75.9 | % | ||||

| Total Same Property operating revenues | 27.5 | 24.5 | 12.3 | % | ||||

| Same Property Expenses | ||||||||

| Same Property operating expenses(d) | 16.8 | 17.1 | (1.7)% | |||||

| Real Property NOI | $ | 10.7 | $ | 7.4 | 44.5 | % | ||

| As of | ||||||||||||

| March 31, 2024 | March 31, 2023 | Change | ||||||||||

| Other Information | ||||||||||||

| Number of properties | 53 | 53 | — | |||||||||

| Sites | ||||||||||||

| UK sites | 16,690 | 16,440 | 250 | |||||||||

| UK transient sites | 3,060 | 3,130 | (70 | ) | ||||||||

| Occupancy(e) | 89.4 | % | 90.7 | % | (1.3)% | |||||||

| Monthly base rent per site | $ | 521 | $ | 481 | $ | 40 | ||||||

(a) Refer to the Definitions and Notes for additional information.

(b) Same Property results for the UK properties reflect constant currency for comparative purposes. UK currency figures in the prior comparative period have been translated at the average exchange rate of $1.2681 USD per Pound sterling, during the quarter ended March 31, 2024.

(c) Percentages are calculated based on unrounded numbers.

(d) Refer to “Utility Revenues” within Definitions and Notes for additional information.

(e) Adjusting for recently delivered and vacant expansion sites, Same Property adjusted occupancy decreased by 40 basis points year over year, to 90.4% at March 31, 2024, from 90.8% at March 31, 2023.

Home Sales Summary

($ in millions, except for average selling price)

| Quarter Ended | ||||||||||

| Financial Information | March 31, 2024 | March 31, 2023 | % Change | |||||||

| MH | ||||||||||

| Home sales | $ | 32.8 | $ | 47.2 | (30.5)% | |||||

| Home cost and selling expenses | 26.2 | 36.0 | (27.2)% | |||||||

| NOI | $ | 6.6 | $ | 11.2 | (41.1)% | |||||

| NOI margin % | 20.1 | % | 23.7 | % | ||||||

| UK(a) | ||||||||||

| Home sales | $ | 36.1 | $ | 39.1 | (7.7)% | |||||

| Home cost and selling expenses | 25.7 | 26.6 | (3.4)% | |||||||

| NOI | $ | 10.4 | $ | 12.5 | (16.8)% | |||||

| NOI margin % | 28.8 | % | 32.0 | % | ||||||

| Total(a) | ||||||||||

| Home sales | $ | 68.9 | $ | 86.3 | (20.2)% | |||||

| Home cost and selling expenses | 51.9 | 62.6 | (17.1)% | |||||||

| NOI | $ | 17.0 | $ | 23.7 | (28.3)% | |||||

| NOI margin % | 24.7 | % | 27.5 | % | ||||||

| Other information | ||||||||||

| Units Sold: | ||||||||||

| MH | 327 | 589 | (44.5)% | |||||||

| UK | 621 | 589 | 5.4 | % | ||||||

| Total home sales | 948 | 1,178 | (19.5)% | |||||||

| Average Selling Price: | ||||||||||

| MH | $ | 100,306 | $ | 80,136 | 25.2 | % | ||||

| UK | $ | 58,132 | $ | 66,384 | (12.4)% | |||||

Operating Statistics for MH and Annual RVs

| Resident Move-outs | |||||||||||||

| % of Total Sites | Number of Move-outs | Leased Sites, Net(b) | New Home Sales | Pre-owned Home Sales | Brokered Re-sales | ||||||||

| 2024 – YTD as of March 31 | 3.9 | % | (a) | 2,290 | 233 | 70 | 257 | 347 | |||||

| 2023 | 3.6 | % | 6,590 | 3,268 | 564 | 2,001 | 2,296 | ||||||

| 2022 | 3.0 | % | 5,170 | 2,922 | 703 | 2,509 | 2,864 | ||||||

(a) Percentage calculated on a trailing 12-month basis.

(b) Net increase in revenue producing sites.

Acquisitions and Dispositions

(amounts in millions, except for *)

| Property Name | Property Type | Number of Properties* | Sites, Wet Slips and Dry Storage Spaces* | Expansion or Development Sites* | State, Province or Country | Total Purchase / Sale Price | Month | ||||||||

| ACQUISITIONS | |||||||||||||||

| First Quarter 2024 | |||||||||||||||

| Port of San Juan(a) | Marina | 1 | 8 | — | PR | $ | — | March | |||||||

| Subsequent to First Quarter 2024 | |||||||||||||||

| Port Milford(b) | Marina | 1 | 92 | — | CT | 4.0 | April | ||||||||

| Oak Leaf | Marina | 1 | 89 | — | CT | 5.0 | April | ||||||||

| Berth One Palm Beach | Marina | 1 | 4 | — | FL | 3.0 | April | ||||||||

| Acquisitions to Date | 4 | 193 | — | $ | 12.0 | ||||||||||

| DISPOSITIONS | |||||||||||||||

| First Quarter 2024 | |||||||||||||||

| Spanish Trails and Sundance | MH | 2 | 533 | — | AZ & FL | $ | 51.7 | February | |||||||

| Dispositions to Date | 2 | 533 | — | $ | 51.7 | ||||||||||

(a) Acquired via ground lease agreement.

(b) In conjunction with this acquisition, the Company issued 19,326 common OP units valued at $2.5million.

Capital Expenditures and Investments

(amounts in millions, except for *)

| Quarter Ended | Year Ended | ||||||||||||||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | December 31, 2022 | |||||||||||||||||||||||||||||||||

| MH / RV | Marina | UK | Total | MH / RV | Marina | UK | Total | MH / RV | Marina | UK | Total | ||||||||||||||||||||||||

| Recurring Capital Expenditures(a) | $ | 11.3 | $ | 15.4 | $ | 3.3 | $ | 30.0 | $ | 51.8 | $ | 35.5 | $ | — | $ | 87.3 | $ | 51.0 | $ | 22.8 | $ | — | $ | 73.8 | |||||||||||

| Non-Recurring Capital Expenditures(a) | |||||||||||||||||||||||||||||||||||

| Lot Modifications | $ | 5.7 | N/A | $ | 1.2 | $ | 6.9 | $ | 54.9 | N/A | $ | — | $ | 54.9 | $ | 39.1 | N/A | $ | — | $ | 39.1 | ||||||||||||||

| Growth Projects | 1.7 | 26.1 | 3.1 | 30.9 | 21.6 | 82.9 | — | 104.5 | 28.4 | 71.1 | — | 99.5 | |||||||||||||||||||||||

| Rebranding | — | N/A | 2.2 | 2.2 | 4.7 | N/A | — | 4.7 | 15.0 | N/A | — | 15.0 | |||||||||||||||||||||||

| Acquisitions | 22.3 | 30.0 | 0.4 | 52.7 | 115.1 | 186.3 | 67.3 | 368.7 | 503.0 | 522.5 | 2,285.1 | 3,310.6 | |||||||||||||||||||||||

| Expansion and Development | 32.2 | 2.5 | 6.4 | 41.1 | 247.4 | 26.0 | 2.9 | 276.3 | 243.8 | 13.9 | 4.1 | 261.8 | |||||||||||||||||||||||

| Total Non-Recurring Capital Expenditures | 61.9 | 58.6 | 13.3 | 133.8 | 443.7 | 295.2 | 70.2 | 809.1 | 829.3 | 607.5 | 2,289.2 | 3,726.0 | |||||||||||||||||||||||

| Total | $ | 73.2 | $ | 74.0 | $ | 16.6 | $ | 163.8 | $ | 495.5 | $ | 330.7 | $ | 70.2 | $ | 896.4 | $ | 880.3 | $ | 630.3 | $ | 2,289.2 | $ | 3,799.8 | |||||||||||

| Other Information | |||||||||||||||||||||||||||||||||||

| Recurring Capex per Site, Slip and Dry Storage Spaces(b)* | $ | 77 | $ | 321 | $ | 182 | $ | 580 | $ | 388 | $ | 867 | N/A | $ | 1,255 | $ | 397 | $ | 582 | N/A | $ | 979 | |||||||||||||

N/A = Not applicable.

(a) Refer to Definitions and Notes for additional information.

(b) Average based on actual number of MH and RV sites, Marina wet slips and dry storage spaces, and UK sites associated with the recurring capital expenditures in each period.

Capitalization Overview

(Shares and units in thousands, dollar amounts in millions, except for *)

| As of | |||||||||

| March 31, 2024 | |||||||||

| Equity and enterprise value | Common Equivalent Shares | Share Price* | Capitalization | ||||||

| Common shares | 124,642 | $ | 128.58 | $ | 16,026.5 | ||||

| Convertible securities | |||||||||

| Common OP units | 2,684 | $ | 128.58 | 345.1 | |||||

| Preferred OP units | 2,617 | $ | 128.58 | 336.5 | |||||

| Diluted shares outstanding and market capitalization(a) | 129,943 | 16,708.1 | |||||||

| Plus: Total debt, per consolidated balance sheet | 7,872.0 | ||||||||

| Total capitalization | 24,580.1 | ||||||||

| Less: Cash and cash equivalents (excluding restricted cash) | (118.9 | ) | |||||||

| Enterprise value(b) | $ | 24,461.2 | |||||||

| Debt | Weighted Average Maturity (in years)* | Debt Outstanding | |||||||

| Mortgage loans payable | 8.9 | $ | 3,465.5 | ||||||

| Secured borrowings on collateralized receivables(b) | 13.9 | 56.1 | |||||||

| Unsecured debt | 4.9 | 4,350.4 | |||||||

| Total carrying value of debt, per consolidated balance sheet | 6.8 | 7,872.0 | |||||||

| Plus: Unamortized deferred financing costs and discounts / premiums on debt | 39.0 | ||||||||

| Total debt(c) | $ | 7,911.0 | |||||||

| Corporate debt rating and outlook | |||||||||

| Moody’s | Baa3 | Stable | ||||||||

| S&P | BBB | Stable | ||||||||

(a) Refer to “Securities” within Definitions and Notes for additional information related to the Company’s securities outstanding.

(b) Refer to “Secured borrowings on collateralized receivables” within Definitions and Notes for additional information.

(c) Refer to “Enterprise Value” and “Net Debt” within Definitions and Notes for additional information.

Summary of Outstanding Debt

(amounts in millions, except for *)

| Quarter Ended | ||||||||

| March 31, 2024 | ||||||||

| Debt Outstanding | Weighted Average Interest Rate(a)* | Maturity Date* | ||||||

| Secured Debt: | ||||||||

| Mortgage loans payable | $ | 3,465.5 | 3.99 | % | Various | |||

| Secured borrowings on collateralized receivables(b) | 56.1 | 8.56 | % | Various | ||||

| Total Secured Debt | 3,521.6 | 4.07 | % | |||||

| Unsecured Debt: | ||||||||

| Senior Credit Facility: | ||||||||

| Revolving credit facilities (in USD)(c) | 1,672.8 | 5.18 | % | April 2026 | ||||

| Other unsecured term loan | 3.9 | 6.47 | % | October 2025 | ||||

| Senior credit facility and other term loan | 1,676.7 | 5.19 | % | |||||

| Senior Unsecured Notes: | ||||||||

| 2028 senior unsecured notes | 447.0 | 2.30 | % | November 2028 | ||||

| 2029 senior unsecured notes | 495.6 | 5.55 | % | January 2029 | ||||

| 2031 senior unsecured notes | 742.6 | 2.70 | % | July 2031 | ||||

| 2032 senior unsecured notes | 592.7 | 3.59 | % | April 2032 | ||||

| 2033 senior unsecured notes | 395.8 | 5.51 | % | January 2033 | ||||

| Total Senior Unsecured Notes | 2,673.7 | 3.78 | % | |||||

| Total Unsecured Debt | 4,350.4 | 4.32 | % | |||||

| Total carrying value of debt, per consolidated balance sheets | 7,872.0 | 4.21 | % | |||||

| Plus: Unamortized deferred financing costs, discounts / premiums on debt, and fair value adjustments(a) | 39.0 | |||||||

| Total debt(d) | $ | 7,911.0 | ||||||

(a)Includes the effect of amortizing deferred financing costs, loan premiums / discounts, and derivatives, as well as fair value adjustments on the Secured borrowings on collateralized receivables.

(b)Refer to “Secured borrowings on collateralized receivables” within Definitions and Notes for additional information.

(c)As of March 31, 2024, the Company’s revolving credit facilities consisted of:

- $150.0 million borrowed on its U.S. line of credit at the Secured Overnight Financing Rate (“SOFR”) plus 85 basis points margin. This $150.0 million is swapped to a weighted average fixed SOFR rate of 4.757% for an all-in fixed rate of 5.707%.

- $1.5 billion (£1.2 billion) borrowed on its GBP and multicurrency lines of credit at the Daily Sterling Overnight Index Average (“SONIA”) base rate, plus 85 basis points margin. As of March 31, 2024, £500.0 million ($631.2 million equivalent) was swapped to a weighted average fixed SONIA rate of 2.924% for an all-in fixed rate of 3.806% inclusive of margin.

- $3.9 million USD equivalent borrowed on its AUD line of credit at the Bank Bill Swap Bid Rate (“BBSY”) plus 85 basis points margin.

(d)Refer to “Enterprise Value” and “Net Debt” within Definitions and Notes for additional information.

(e)

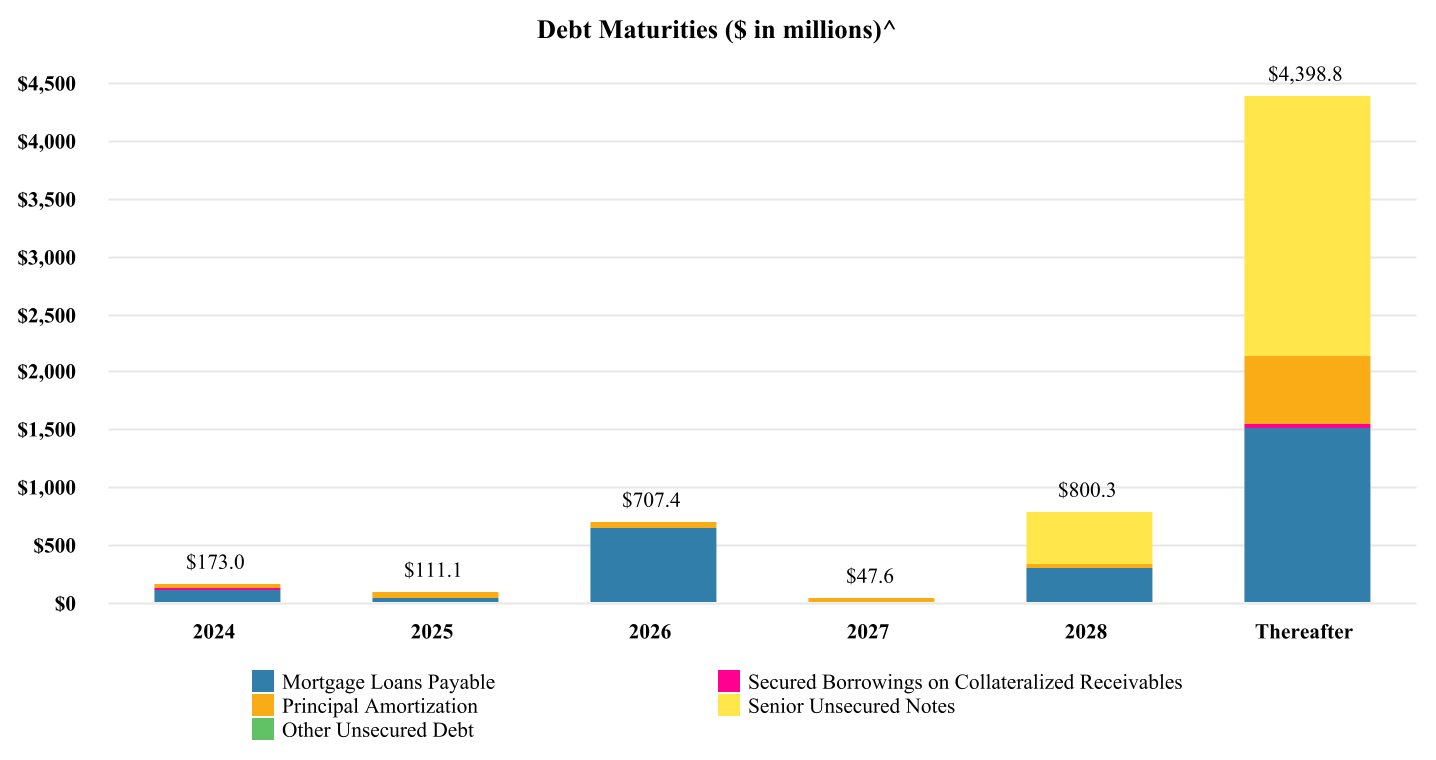

Debt Maturities(a)

(amounts in millions, except for *)

| Year | Mortgage Loans Payable(b) | Secured Borrowings on Collateralized Receivables(c)(d) | Principal Amortization | Senior Credit Facility | Senior Unsecured Notes | Other Unsecured Debt | Total | ||||||||||||||

| 2024 | $ | 128.8 | $ | 1.7 | $ | 42.5 | $ | — | $ | — | $ | — | $ | 173.0 | |||||||

| 2025 | 50.5 | 2.5 | 54.2 | — | — | 3.9 | 111.1 | ||||||||||||||

| 2026 | 658.4 | 2.7 | 46.3 | 1,672.8 | — | — | 2,380.2 | ||||||||||||||

| 2027 | 4.0 | 2.9 | 40.7 | — | — | — | 47.6 | ||||||||||||||

| 2028 | 303.8 | 3.1 | 43.4 | — | 450.0 | — | 800.3 | ||||||||||||||

| Thereafter | 1,525.2 | 39.7 | 583.9 | — | 2,250.0 | — | 4,398.8 | ||||||||||||||

| Total | $ | 2,670.7 | $ | 52.6 | $ | 811.0 | $ | 1,672.8 | $ | 2,700.0 | $ | 3.9 | $ | 7,911.0 | |||||||

(a) Debt maturities include the unamortized deferred financing costs, discount / premiums, and fair value adjustments associated with outstanding debt.

(b) For the Mortgage loan payables maturing between 2024 – 2028:

| 2024 | 2025 | 2026 | 2027 | 2028 | ||||||||||

| Weighted average interest rate | 4.03 | % | 4.04 | % | 3.97 | % | 4.34 | % | 4.04 | % |

(c) Balance at March 31, 2024 excludes fair value adjustments of $3.5million.

(d) Refer to “Secured borrowings on collateralized receivables” within Definitions and Notes for additional information.

^ Excludes the Company’s borrowings under its senior credit facility.

Debt Analysis

| As of | |||||

| March 31, 2024 | |||||

| Select Credit Ratios | |||||

| Net debt / TTM recurring EBITDA(a) | 6.1 x | ||||

| Net debt / enterprise value | 31.7 | % | |||

| Net debt / gross assets | 37.8 | % | |||

| Unencumbered assets / total assets | 76.8 | % | |||

| Floating rate debt / total debt(b) | 11.3 | % | |||

| Coverage Ratios | |||||

| TTM Recurring EBITDA(a) / interest | 3.7 x | ||||

| TTM Recurring EBITDA(a) / interest + preferred distributions + preferred stock distribution | 3.7 x | ||||

| Senior Credit Facility Covenants | Requirement | ||||

| Maximum leverage ratio | <65.0 % | 34.2 | % | ||

| Minimum fixed charge coverage ratio | >1.40 x | 3.08 x | |||

| Maximum secured leverage ratio | <40.0 % | 12.9 | % | ||

| Senior Unsecured Note Covenants | Requirement | ||||

| Total debt / total assets | ≤60.0 % | 41.5 | % | ||

| Secured debt / total assets | ≤40.0 % | 18.5 | % | ||

| Consolidated income available for debt service / debt service | ≥1.50 x | 3.84 x | |||

| Unencumbered total asset value / total unsecured debt | ≥150.0 % | 334.6 | % | ||

(a) Refer to page 8 for additional detail on the Company’s TTM Recurring EBITDA.

(b) Percentage includes the impact of hedge activities.

Definitions and Notes

Acquisition and Other Transaction Costs – In the Company’s Reconciliation of Net Loss Attributable to SUI Common Shareholders to Core FFO on page 6, ‘Acquisition and other transaction costs’ represent (a) nonrecurring integration expenses associated with acquisitions during the quarters ended March 31, 2024 and 2023, (b) costs associated with potential acquisitions that will not close, (c) expenses incurred to bring recently acquired properties up to the Company’s operating standards, including items such as tree trimming and painting costs that do not meet the Company’s capitalization policy, and other non-recurring transaction costs, and (d) other non-recurring transactions.

Capital Expenditures and Investment Activity – The Company classifies its investments in properties into the following categories:

- Recurring Capital Expenditures – Property recurring capital expenditures are necessary to maintain asset quality, including purchasing and replacing items used to operate the communities and marinas. Recurring capital expenditures at the Company’s MH, RV and UK properties include major road, driveway and pool improvements; clubhouse renovations; adding or replacing streetlights; playground equipment; signage; maintenance facilities; manager housing and property vehicles. Recurring capital expenditures at the marinas include dredging, dock repairs and improvements, and equipment maintenance and upgrades. The minimum capitalized amount is five hundred dollars.

- Non-Recurring Capital Expenditures – The following investment and reinvestment activities are non-recurring in nature:

- Lot Modifications – Lot modification capital expenditures are incurred to modify the foundational structures required to set a new home after a previous home has been removed. These expenditures are necessary to create a revenue stream from a new site renter and often improve the quality of the community. Other lot modification expenditures include land improvements added to annual RV sites to aid in the conversion of transient RV guests to annual contracts. See page 13 for move-out rates.

- Growth Projects – Growth projects consist of revenue-generating or expense-reducing activities at the properties. These include, but are not limited to, utility efficiency and renewable energy projects, site, slip or amenity upgrades, such as the addition of a garage, shed or boat lift, and other special capital projects that substantiate an incremental rental increase.

- Rebranding – Rebranding includes new signage at the Company’s RV communities and costs of building an RV mobile application and updated website.

- Acquisitions – Total acquisition investments represent the purchase price paid for operating properties (detailed for the current calendar year on page 14), the purchase price paid for land parcels for future ground-up development and expansions activities, and any capital improvements identified during due diligence needed to bring acquired properties up to the Company’s operating standards.

Capital improvements subsequent to acquisition often require 24 to 36 months to complete after closing. At MH, RV and UK properties, capital improvements include upgrading clubhouses; landscaping; new street light systems; new mail delivery systems; pool renovations including larger decks, heaters and furniture; new maintenance facilities; lot modifications; and new signage including main signs and internal road signs. Capital improvements at Marina properties primarily include improvements to rooms, renovation of restaurant facilities, pools and fitness centers.

For the quarter ended March 31, 2024, the components of total acquisition investment are as follows (in millions):

| Quarter Ended March 31, 2024 | ||||||||||||

| MH and RV | Marina | UK | Total | |||||||||

| Purchase price of land acquisitions (including capitalized transaction costs)(a) | $ | 15.8 | $ | — | $ | — | $ | 15.8 | ||||

| Capital improvements to recent property acquisitions | 6.1 | 16.0 | 0.4 | 22.5 | ||||||||

| Other acquisitions | 0.4 | 14.0 | — | 14.4 | ||||||||

| Total Acquisition Investments | $ | 22.3 | $ | 30.0 | $ | 0.4 | $ | 52.7 | ||||

(a) Includes the value allocated to infrastructure improvements associated with acquired land, when applicable.

- Expansions and Developments – Expansion and development expenditures consist primarily of construction costs such as roads, activities, and amenities, and costs necessary to complete site improvements, such as driveways, sidewalks and landscaping at the Company’s MH, RV and UK communities. Expenditures also include costs to rebuild after damage has been incurred at MH, RV, Marina or UK properties, and research and development.

Enterprise Value – Equals total equity market capitalization, plus total indebtedness reported on the Company’s balance sheet and less cash and cash equivalents (excluding restricted cash).

GAAP – U.S. Generally Accepted Accounting Principles.

Home Sales Contribution to FFO – The reconciliation of NOI from home sales to FFO from home sales for the quarter ended March 31, 2024 is as follows (in millions):

| Quarter Ended March 31, 2024 | |||||||||||

| MH | UK | Total | |||||||||

| Home Sales NOI | $ | 6.6 | $ | 10.4 | $ | 17.0 | |||||

| Gain on dispositions of assets, net | (5.2 | ) | (0.2 | ) | (5.4 | ) | |||||

| FFO Contribution from home sales | $ | 1.4 | $ | 10.2 | $ | 11.6 | |||||

Interest Expense – The following is a summary of the components of the Company’s interest expense (in millions):

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| Interest on Secured debt, Senior unsecured notes, Senior Credit Facility, Unsecured Term Loan and interest rate swaps | $ | 83.9 | $ | 72.4 | |||

| Lease related interest expense | 3.5 | 3.5 | |||||

| Amortization of deferred financing costs, debt / (premium) or discounts and (gains) / losses on hedges | 1.8 | 1.5 | |||||

| Senior credit facility commitment fees and other finance related charges | 2.0 | 1.7 | |||||

| Capitalized interest expense | (2.7 | ) | (2.5 | ) | |||

| Interest Expense Before Interest on Secured borrowings | 88.5 | 76.6 | |||||

| Interest expense on Secured borrowings on collateralized receivables | 1.2 | — | |||||

| Interest Expense, per Consolidated Statements of Operations | $ | 89.7 | $ | 76.6 | |||

Nareit – The National Association of Real Estate Investment Trusts is the worldwide representative voice for REITs and real estate companies with an interest in U.S. real estate and capital markets. More information is available at www.reit.com.

Net Debt – The carrying value of debt, plus, unamortized premiums, discounts and deferred financing costs, less, unrestricted cash (i.e., cash and cash equivalents, excluding restricted cash).

Other adjustments, net – In the Company’s Reconciliation of Net Loss Attributable to SUI Common Shareholders to Core FFO on page 6, ‘Other adjustments, net’ consists of the following (in millions):

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| Litigation settlement gain | $ | (8.1 | ) | $ | — | ||

| Long term lease termination expense | — | 0.6 | |||||

| Severance costs | 0.5 | — | |||||

| Deferred tax benefit | (5.7 | ) | (4.6 | ) | |||

| Accelerated deferred compensation amortization | 0.2 | 0.4 | |||||

| ERP implementation expense | 0.7 | ||||||

| Other adjustments, net | $ | (12.4 | ) | $ | (3.6 | ) | |

Other income / (expense), net – In the Company’s Consolidated Statements of Operations on page 5, ‘Other income / (expense), net’ consists of the following (in millions):

| Quarter Ended | |||||||

| March 31, 2024 | March 31, 2023 | ||||||

| Litigation settlement gain | $ | 8.1 | $ | — | |||

| Long term lease termination expense | — | (0.6 | ) | ||||

| Repair reserve on repossessed homes | (0.1 | ) | (0.4 | ) | |||

| Gain on remeasurement of Collateralized receivables | 1.6 | — | |||||

| Loss on remeasurement of Secured borrowings on collateralized receivables | (1.6 | ) | — | ||||

| Other income / (expense), net | $ | 8.0 | $ | (1.0 | ) | ||

Same Property – The Company defines Same Properties as those the Company has owned and operated continuously since at least January 1, 2023. Same properties exclude ground-up development properties, acquired properties and properties sold after December 31, 2022. The Same Property data may change from time-to-time depending on acquisitions, dispositions, management discretion, significant transactions or unique situations.

Secured borrowings on collateralized receivables – This is a transferred asset transaction which has been classified as collateralized receivables and the cash received from this transaction has been classified as secured borrowings. The interest income and interest expense accrue at the same amount. The Company elected to fair value the collateralized receivables and the secured borrowings under ASC 820, “Fair Value Measurements and Disclosures.” As a result, the balance of collateralized receivables and related secured borrowings are net of fair value adjustments.

Securities – The Company had the following securities outstanding as of March 31, 2024:

| Number of Units / Shares Outstanding (in thousands) | Conversion Rate(a) | If Converted to Common shares (in thousands)(b) | Issuance Price Per Unit | Annual Distribution Rate | |||||||

| Non-Convertible Securities | |||||||||||

| Common shares | 124,642 | N/A | N/A | N/A | $3.76(c) | ||||||

| Convertible Securities Classified as Equity | |||||||||||

| Common OP units | 2,684 | 1.0000 | 2,684 | N/A | Mirrors common share distributions | ||||||

| Preferred OP Units | |||||||||||

| Series A-1 | 192 | 2.4390 | 468 | $ | 100.00 | 6.00 | % | ||||

| Series A-3 | 40 | 1.8605 | 75 | $ | 100.00 | 4.50 | % | ||||

| Series C | 305 | 1.1100 | 339 | $ | 100.00 | 5.00 | % | ||||

| Series D | 489 | 0.8000 | 391 | $ | 100.00 | 4.00 | % | ||||

| Series E | 80 | 0.6897 | 55 | $ | 100.00 | 5.50 | % | ||||

| Series F | 90 | 0.6250 | 56 | $ | 100.00 | 3.00 | % | ||||

| Series G | 206 | 0.6452 | 133 | $ | 100.00 | 3.20 | % | ||||

| Series H | 581 | 0.6098 | 355 | $ | 100.00 | 3.00 | % | ||||

| Series J | 238 | 0.6061 | 144 | $ | 100.00 | 2.85 | % | ||||

| Series K | 1,000 | 0.5882 | 588 | $ | 100.00 | 4.00 | % | ||||

| Series L | 20 | 0.6250 | 13 | $ | 100.00 | 3.50 | % | ||||

| Total | 3,241 | 2,617 | |||||||||

| Total convertible securities outstanding | 5,925 | 5,301 | |||||||||

(a) Exchange rates are subject to adjustment upon stock splits, recapitalizations and similar events. The exchange rates of certain series of OP units are approximated to four decimal places.

(b) Calculation may yield minor differences due to fractional shares paid in cash to the shareholder at conversion.

(c) Annual distribution is based on the last quarterly distribution annualized.

Share – In addition to reporting net income on a diluted basis (“EPS”), the Company reports FFO and Core FFO on a per common share and dilutive convertible securities basis (per “Share”). For the periods presented below, the Company’s diluted weighted average common shares outstanding for EPS and FFO are as follows:

| Quarter Ended | |||

| March 31, 2024 | March 31, 2023 | ||

| Diluted Weighted Average Common Shares Outstanding – EPS | As Restated | ||

| Weighted average common shares outstanding – Basic | 123.6 | 123.3 | |

| Dilutive restricted stock | 0.3 | 0.4 | |

| Common and preferred OP units dilutive effect | 2.7 | 2.5 | |

| Weighted Average Common Shares Outstanding – Diluted | 126.6 | 126.2 | |

| Diluted Weighted Average Common Shares Outstanding – FFO | |||

| Weighted average common shares outstanding – Basic | 123.7 | 123.3 | |

| Restricted stock | 0.3 | 0.4 | |

| Common OP units | 2.7 | 2.4 | |

| Common stock issuable upon conversion of certain preferred OP units | 2.0 | 2.1 | |

| Weighted Average Common Shares Outstanding – Diluted | 128.7 | 128.2 | |

Utility Revenues – In its Consolidated Statements of Operations and its total portfolio presentation of real property operating results, the Company includes the following utility reimbursement revenues in real property revenues (excluding transient):

| Quarter Ended | |||||

| Consolidated Portfolio | March 31, 2024 | March 31, 2023 | |||

| Utility reimbursement revenues | |||||

| MH | $ | 18.5 | $ | 18.5 | |

| RV | 4.2 | 4.2 | |||

| Marina | 5.9 | 5.3 | |||

| UK | 4.8 | 4.6 | |||

| Total | $ | 33.4 | $ | 32.6 | |

For its presentation of Same Property results on page 10 and page 12, the Company nets the following utility revenues (which include utility reimbursement revenues from residents) against related utility expenses in Same Property operating expenses:

| Quarter Ended | |||||

| Same Property Portfolio | March 31, 2024 | March 31, 2023 | |||

| Utility revenues netted against related utility expenses | |||||

| MH | $ | 18.4 | $ | 18.4 | |

| RV | 4.1 | 4.1 | |||

| Marina | 5.5 | 5.2 | |||

| UK | 4.7 | 4.8 | |||

| Total | $ | 32.7 | $ | 32.5 | |

Non-GAAP Supplemental Measures

Investors and analysts following the real estate industry use non-GAAP supplemental performance measures, including net operating income (“NOI”), earnings before interest, tax, depreciation and amortization (“EBITDA”) and funds from operations (“FFO”) to assess REITs. The Company believes that NOI, EBITDA and FFO are appropriate measures given their wide use by and relevance to investors and analysts. Additionally, NOI, EBITDA and FFO are commonly used in various ratios, pricing multiples, yields and returns and valuation calculations used to measure financial position, performance and value.

NOI provides a measure of rental operations that does not factor in depreciation, amortization and non-property specific expenses such as general and administrative expenses.

EBITDA provides a further measure to evaluate ability to incur and service debt; EBITDA also provides further measures to evaluate the Company’s ability to fund dividends and other cash needs.

FFO, reflecting the assumption that real estate values rise or fall with market conditions, principally adjusts for the effects of GAAP depreciation and amortization of real estate assets.

- Net Operating Income (“NOI”)

- Total Portfolio NOI – The Company calculates NOI by subtracting property operating expenses and real estate taxes from operating property revenues. NOI is a non-GAAP financial measure that the Company believes is helpful to investors as a supplemental measure of operating performance because it is an indicator of the return on property investment and provides a method of comparing property performance over time. The Company uses NOI as a key measure when evaluating performance and growth of particular properties and / or groups of properties. The principal limitation of NOI is that it excludes depreciation, amortization, interest expense and non-property specific expenses such as general and administrative expenses, all of which are significant costs. Therefore, NOI is a measure of the operating performance of the properties of the Company rather than of the Company overall. The Company believes that NOI provides enhanced comparability for investor evaluation of properties performance and growth over time.

The Company believes that GAAP net income (loss) is the most directly comparable measure to NOI. NOI should not be considered to be an alternative to GAAP net income (loss) as an indication of the Company’s financial performance or GAAP cash flow from operating activities as a measure of the Company’s liquidity; nor is it indicative of funds available for the Company’s cash needs, including its ability to make cash distributions. Because of the inclusion of items such as interest, depreciation and amortization, the use of GAAP net income (loss) as a performance measure is limited as these items may not accurately reflect the actual change in market value of a property, in the case of depreciation and in the case of interest, may not necessarily be linked to the operating performance of a real estate asset, as it is often incurred at a parent company level and not at a property level.